Independent auditor’s report

To: the general meeting and Supervisory Board of Coöperatief Deloitte U.A.

A. Report on the audit of the financial statements 2023/2024 included in the Integrated Annual Report

Our opinion

We have audited the financial statements 2023/2024 of Coöperatief Deloitte U.A. ('the Group') based in Rotterdam, the Netherlands. The financial statements comprise the consolidated financial statements and the company financial statements.

WE HAVE AUDITED | OUR OPINION |

The consolidated financial statements comprise:

| In our opinion, the accompanying consolidated financial statements give a true and fair view of the financial position of Coöperatief Deloitte U.A. as at May 31, 2024, and of its result and its cash flows for 2023/2024 in accordance with International Financial Reporting Standards as adopted by the European Union (EU-IFRS) and with Part 9 of Book 2 of the Dutch Civil Code. |

The company financial statements comprise:

| In our opinion, the accompanying company financial statements give a true and fair view of the financial position of Coöperatief Deloitte U.A. as at 31 May 2024 and of its result for the year then ended in accordance with Part 9 of Book 2 of the Dutch Civil Code. |

Basis for our opinion

We conducted our audit in accordance with Dutch law, including the Dutch Standards on Auditing. Our responsibilities under those standards are further described in the ‘Our responsibilities for the audit of the financial statements section of our report.

We are independent of Coöperatief Deloitte U.A. in accordance with the EU Regulation on specific requirements regarding statutory audit of public-interest entities, the Wet toezicht accountantsorganisaties (Wta, Audit firms supervision act), the Verordening inzake de onafhankelijkheid van accountants bij assurance-opdrachten (ViO, Code of Ethics for Professional Accountants, a regulation with respect to independence). Furthermore, we have complied with the Verordening gedrags- en beroepsregels accountants (VGBA, Dutch Code of Ethics).

We believe the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

B. Information in support of our opinion

By performing the procedures mentioned above for group entities, together with additional procedures at group level, we have been able to obtain sufficient and appropriate audit evidence about the group’s financial information to provide an opinion on the consolidated financial statements.

Audit approach going concern

The Executive Board prepared the (consolidated) financial statements of Coöperatief Deloitte U.A. on the assumption that the entity is a going concern and that it will continue all its operations for at least twelve months from the date of preparation of the financial statements.

As explained in the section 'Going concern' in note 1 of the financial statements, management has carried out a going concern assessment and concluded positively on the entity’s ability to continue as a going concern. Our procedures to evaluate the going concern assessment of management included, amongst others:

-

Considering whether management identified events or conditions that may cast significant doubt on the entity’s ability to continue as a going concern.

-

Considering whether management's going concern assessment included all relevant information of which we were aware as a result of our audit and inquired with the Executive Board regarding the most important assumptions underlying its assessment.

-

Assessing managements’ financial forecasts prepared for a period of at least 12 months from the date of these financial statements. This included the consideration of the reasonableness of key underlying assumptions by reference to current and future expected operating and capital expenditure.

-

Analysing the financial position per balance sheet date in relation to the financial position per prior year balance sheet date to assess whether events or circumstances exist that may lead to a going concern risks beyond the period of the management’s assessment;

-

Performing inquiries of management as to its knowledge of going concern risks beyond the period of management's assessment.

-

Evaluating the adequacy of disclosures made in the financial statements in respect of going concern.

These audit procedures did not lead to any material findings regarding the going concern assumption of the Company, or result in outcomes contrary to the Executive Board’s assumptions and judgments used in the application of the going concern assumption.

Audit approach fraud risks and non-compliance with laws and regulations

We identified and assessed the risks of material misstatements of the financial statements due to fraud and non-compliance with laws and regulations.

During our audit we obtained an understanding of the Group and its environment and the components of the system of internal control, including the risk assessment process and management’s process for responding to the risks of fraud and monitoring the system of internal control and how the Supervisory Board exercises oversight, as well as the outcomes.

We refer to section ‘Executive Board highlights, lessons learned and outlook’ of the Executive Board report for the Executive Board’s fraud risk assessment and section ‘Report from the Supervisory Board’ of the Supervisory Board report in which the Supervisory Board reflects on this fraud risk assessment.

We evaluated the design and relevant aspects of the system of internal control and in particular the fraud risk assessment, as well as among others the code of conduct, whistle blower procedures and incident registration. We asked members of the Executive Board as well as the compliance officer, finance department, the legal counsel and the Supervisory Board whether they are aware of any actual or suspected fraud. This did not result in signals of actual or suspected fraud that may lead to a material misstatement. For further reference on the answer sharing case we refer to the section key audit matters. We evaluated the design and the implementation and, where considered appropriate, tested the operating effectiveness, of internal controls designed to mitigate fraud risks.

We performed risk assessment procedures to identify potential risks of material misstatements due to fraud and non-compliances with laws and regulations. As part of this work we evaluated the Group’s risk assessment and performed inquiries with management and those charged with governance. We also specifically evaluated whether fraud risk factors are present based on the framework of the fraud triangle during several team discussions and considered any unusual or unexpected relationships based on analytical procedures. As part of this assessment, we specifically assessed how fraud risks can arise in the revenue recognition as part of the unbilled revenue process and reflected this in our risk assessment and audit approach.

Following these procedures, and the presumed risks under the prevailing audit standards, we considered the (presumed) fraud risks related to management override of controls and the risk related to the overstatement of (unbilled) revenues. We consider these fraud risks to also be prevalent as a result of the nature of the Group, where the compensation of partners and senior management personnel are driven and based on the annual profits achieved. The partners/senior management therefore might have pressure or incentives to unjustly modify certain aspects of the financial statements in order to increase the profits achieved with the aim to increase their respective compensation. This would especially be relevant for financial statement areas such as unbilled revenue, advanced billings to customers and provisions, such as the professional liability provision or other areas involving significant estimates.

In relation to our risk assessment on non-compliance with laws and regulation, we performed procedures to obtain an understanding of the legal and regulatory frameworks that are applicable for Coöperatief Deloitte U.A.. The potential effect of laws and regulations on the financial statements varies considerably. Resulting from our risk assessment procedures, we considered adherence to (corporate) tax law and financial reporting with a direct effect on the financial statements as an integrated part of our audit procedures to the extent these are material for the financial statements. Furthermore, based on updated risk assessment procedures and in the context of non-compliance risks, we identified a key audit matter on the answer sharing case.

In addition to the aforementioned laws and regulation, Coöperatief Deloitte U.A.is subject to other laws and regulations where the consequences of non-compliance could have a material effect on amounts and/or disclosures in the financial statements, for instance through imposing fines or litigation. Examples of such other laws and regulations are those relating to the supervision of the Financial Market Authority (AFM) based on the Wta and data privacy laws. Auditing standards limit the required audit procedures to identify non-compliance with these laws and regulations to enquiry of the directors and other management and inspection of regulatory and legal correspondence, if any. Therefore, if a breach of operational regulations is not disclosed to us or evident from relevant correspondence, an audit will not detect such breaches.

Our audit procedures to respond to the risk of management override and identify potential other fraud elements include, amongst others:

-

We inquired the procedures for compliance with laws and regulations with relevant personnel, the Executive Board and the Supervisory Board, the Reputation & Risk Leader and the Ethics Officer.

-

We inspected minutes of meetings of the Executive Board and the Supervisory Board.

-

We inspected correspondence with regulators.

-

We evaluated the design and the implementation and, where considered appropriate, tested the operating effectiveness of internal controls that mitigate fraud risks.

-

Supplementary to reliance on the internal controls, we performed substantive audit procedures, including detailed testing of journal entries with a risk-based approach.

-

We reviewed significant accounting estimates for biases and evaluated whether the circumstances producing the bias, if any, represent a risk of material misstatement due to fraud. As part of this we performed a retrospective review and evaluated the judgements and decisions made by management in making the estimates in the current year.

-

We remained alert for indications of fraud throughout our other audit procedures and evaluated whether identified findings or misstatements were indicative of fraud.

-

We assessed matters reported on the Group’s whistleblowing and complaints procedures and assessed, where deemed necessary, the results of management’s follow-up of such matters.

-

We performed an assessment of any significant extraordinary events outside of the normal course of business

-

We obtained written representations that all known instances of (suspected) fraud or non-compliance with laws and regulations have been disclosed to us.

-

We evaluated whether final analytical procedures performed near the end of the audit, when forming an overall conclusion as to whether the financial statements are consistent with our understanding of the Group, indicate a previously unrecognized risk of material misstatement due to fraud.

Our response in addressing the presumed fraud risks on revenue recognition is related to the valuation of unbilled services and advance billings to customers is detailed in our key audit matters.

Our audit procedures in relation to non-compliance with laws and regulations notably consists of:

-

We inquired the procedures for compliance with laws and regulations with relevant personnel, the Executive Board and Supervisory Board, the Reputation & Risk Leader and the Ethics Officer.

-

We inspected minutes of meetings of the Executive Board and the Supervisory Board.

-

We inspected correspondence with regulators.

-

We obtained sufficient appropriate audit evidence regarding compliance with the provisions of those laws and regulations generally recognised to have a direct effect on the determination of material amounts and disclosures in the financial statements, where we also included a specialist in the area of corporate tax law.

-

We performed limited procedures in relation to other laws and regulations, i.e. we performed inquiries with management and those charged with governance as to whether the Group is in compliance with such laws and regulations and we inspected correspondence, if any, with the relevant authorities.

-

During the audit, we remained alert to the possibility that other audit procedures applied may bring instances of non-compliance or suspected non-compliance with laws and regulations to our attention.

-

We obtained management representation that all known instances of non-compliance or suspected non-compliance with laws and regulations whose effects should be considered when preparing the Integrated Annual Report are adequately disclosed in the financial statements.

We incorporated elements of unpredictability in our audit. We also considered the outcome of our other audit procedures and evaluated whether any findings were indicative of fraud or non-compliance.

We considered available information and made enquiries of relevant executives, directors (including internal audit, legal, risk) and the Supervisory Board.

The audit procedures described above have resulted in sufficient and appropriate audit evidence to mitigate the potential fraud risks and non-compliance risks. Our audit procedures did not lead to indications or suspicions for fraud potentially resulting in material misstatements. In respect of the answer sharing case, we refer to the key audit matter.

For an overview of our responsibilities and those of the management regarding the financial statements and the risks of fraud and non-compliance, we refer to section D of this report.

Our key audit matters

Key audit matters are those matters that, in our professional judgement, were of most significance in our audit of the financial statements and the other (integrated) information. We have communicated the key audit matters to the Audit & Finance Committee and the Supervisory Board. The key audit matters are not a comprehensive reflection of all matters discussed.

These matters were addressed in the context of our audit of the financial statements and the other (integrated) information as a whole and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

VALUATION OF UNBILLED SERVICES AND ADVANCE BILLINGS TO CUSTOMERS | OUR AUDIT APPROACH |

As at May 31, 2024, the recognised unbilled services (contract assets) amounts to € 123 million. Refer to note 3.2 - Unbilled services and advance billings to customers.

| We evaluated the design and tested implementation of both automated and manual internal controls within the organisation relating to the valuation of the unbilled revenues and advance billings to customers.

Furthermore, we performed substantive audit procedures on specific elements not yet fully addressed by aforementioned procedures, i.e. back-testing of specific items, cut-off testing including realisation of success fees, onerous contracts and (non) chargeable hours.

|

VALUATION OF PROFESSIONAL LIABILITY PROVISION | OUR AUDIT APPROACH |

The Group is involved in a number of disputes which may give rise to claims. Refer to note 8.2 – Provisions and note 8.3 – Commitments and guarantees for the disclosures with respect to such claims and legal proceedings.

| In addition to testing the design and operating effectiveness of the provisional indemnity claims process and related control procedures, the audit procedures mainly comprised of substantive audit procedures. These procedures notably consisted of:

|

IMPACT OF THE ANSWER SHARING CASE ON THE ACCOUNTING AND DISCLOSURES IN THE INTEGRATED REPORT | OUR AUDIT APPROACH |

Refer to section ‘Executive Board highlights, lessons learned and outlook’ of the Integrated Annual Report and note 8.2 of the financial statements. As a result of incidents involving misconduct on exams at audit firms and at the request of the AFM, Deloitte initiated an investigation into the internal learning culture and learning behaviours of its professionals. The internal investigation is supported by in- and external advisors. The investigation covers all mandatory internal and external learning activities in 2018 up to and including 2023 across the organisation. Based on the preliminary findings, the status of the ongoing investigation, and other facts and circumstances deemed relevant, including but not limited to publicly available information from other global investigations on learning culture and behaviours, the Group recognised a (short-term) provision in the financial statements. Further details, including the calculation of the amount of the provision are not disclosed in the financial statements in accordance with the provisions of IAS 37.92. Impact of the answer sharing case is a key audit matter based on the sensitivity, judgement and complexity of the case. | We inspected letters from the PCAOB, AFM and held conversations with external legal and internal forensic advisors and read (intermediate) reports prepared by Deloitte’s forensic and data analytical experts. We evaluated the objectivity, competency and capabilities of the experts involved. We gained insight into their work by evaluating the scope and extent of their work together with forensic experts from Deloitte. We assessed the (intermediate) results of their work, asked questions, received answers and explanations. Conclusions were discussed with the experts, members of the Executive Board and the Supervisory Board. We evaluated the appropriateness of the work performed and the findings thereon, including provisional results on root cause analysis and remedial measures, in the context of the financial statements audit. We assessed the Group’s position paper and evaluated all other information provided by management to assess the appropriateness of management’s (point) estimate in a range of potential financial outcomes of the claim provision. We assessed management’s assumptions for determining the provision, using an internally set up panel of legal, risk and accounting experts. We assessed the accounting disclosures in note 8.2 of the financial statement and the section ‘Executive Board highlights, lessons learned and outlook’ of the Integrated Annual Report on this matter, considering the audit evidence obtained from the ongoing investigations, findings noted and communication with the regulators. The presentation and disclosure is deemed appropriate and in accordance with IAS 37 requirements. Based on our procedures, we found the Executive Board’s assumptions underlying the provision to be supported by available evidence and we did not identify material exceptions in the disclosures related to the answer sharing case. |

C. Report on other information included in the Integrated Annual Report

D. Report on other legal and regulatory requirements

Engagement

We were engaged by the Supervisory Board as auditor of Coöperatief Deloitte U.A. for the audit of the financial year ended May 31, 2024, on September 13, 2023.

No prohibited non-audit services

We have not provided prohibited non-audit services as referred to in Article 5(1) of the EU Regulation on specific requirements regarding statutory audit of public-interest entities.

E. Description of responsibilities regarding the financial statements

Responsibilities of Executive Board and the Supervisory Board for the financial statements

The Executive Board is responsible for the preparation and fair presentation of the financial statements in accordance with EU-IFRS and Part 9 of Book 2 of the Dutch Civil Code.

Furthermore, the Executive Board is responsible for such internal control as it determines necessary to enable the preparation of the financial statements that are free from material misstatement, whether due to fraud or error.

As part of the preparation of the financial statements, the Executive Board is responsible for assessing the Company’s ability to continue as a going concern. Based on the financial reporting frameworks mentioned, the Executive Board should prepare the financial statements using the going concern basis of accounting, unless the Executive Board either intends to liquidate the company or to cease operations, or has no realistic alternative but to do so. The Executive Board should disclose events and circumstances that may cast significant doubt on the company’s ability to continue as a going concern in the financial statements.

The Supervisory Board is responsible for overseeing Coöperatief Deloitte U.A.’s reporting process.

Our responsibilities for the audit of the financial statements

Our responsibility is to plan and perform the audit engagement in a manner that allows us to obtain sufficient and appropriate audit evidence for our opinion.

Our audit has been performed with a high, but not absolute, level of assurance, which means we may not detect all material errors and fraud during our audit.

Misstatements may arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements. The materiality affects the nature, timing and extent of our audit procedures and the evaluation of the effect of identified misstatements on our opinion.

We exercised professional judgement and maintained professional skepticism throughout the audit, in accordance with Dutch Standards on Auditing, ethical requirements and independence requirements. Our audit on the financial statements included among others:

-

identifying and assessing the risks of material misstatement of the financial statements, whether due to fraud or error, designing and performing audit procedures responsive to those risks, and obtaining audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control;

-

obtaining an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control;

-

evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management;

-

concluding on the appropriateness of management’s use of the going concern basis of accounting, and based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the entity’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause a company to cease to continue as a going concern;

-

evaluating the overall presentation, structure and content of the financial statements, including the disclosures; and

-

evaluating whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

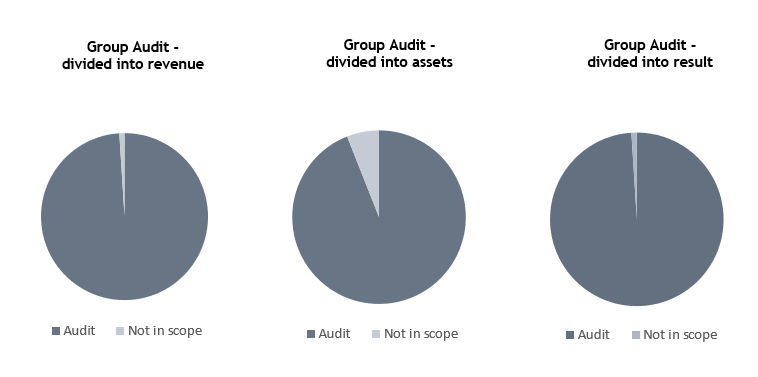

As we are ultimately responsible for the opinion, we are also responsible for directing, supervising and performing the group audit. In this respect we determined the nature and extent of the audit procedures to be carried out for group entities. Decisive were the size and/or the risk profile of the group entities or operations. On this basis, we selected group entities for which an audit or review had to be carried out on the complete set of financial information or specific items.

We communicated with the Supervisory Board regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant findings in internal control that we identified during our audit.

We provide the Supervisory Board with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with the Supervisory Board, we determine the key audit matters to entail those matters that were of most significance in the audit of the financial statements. We described these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determined that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

For and on behalf of BDO Audit & Assurance B.V.,

Rotterdam, July 18, 2024

Drs. A. Thomson RA